A brief guide to the battered energy complex and the clues to look for before buying.

Oil has been even more important than usual in the past few months for financial markets. Slowing demand growth, rising U.S. production, and cyclical issues in emerging markets lead to a persistent supply glut (thanks to Saudi tactics at least in part) and pushed prices down by more than 70%.

The decline caused bankruptcy fears (not unfounded ones) concerning over-leveraged and borderline unsustainable producers with some analysts expecting as much as one-third of the O&G complex going bust.

After dipping below $30, for a 13-year low, WTI is possibly building a durable bottom amid the horrible sentiment. Recent news on the agreement between Saudi-Arabia and Russia on freezing production propelled oil higher and although it’s hard to imagine that these nations will keep their promises, this could be a good “excuse” for the market to stage a meaningful rally.

Yields of lower quality bonds (as seen above) in the sector skyrocketed with some contagion to other industries as well. Coupled with the global slowdown in economic growth (and the new Bail-in directive in Europe) banks and other financials also got sold as the exposures and the long-term consequences could jeopardize profitability in the highly leveraged financial system of the post-crisis era.

Common sense would tell us that falling oil prices are good for most of the economies and consumers. How come that it still can lead to a crisis in confidence worldwide?

Let’s take look at the most relevant effects of the slump:

- A drastic slowdown in oil producing countries. Devaluation of related (and unpegged) currencies.

- Net outflows from connected Sovereign Wealth Funds (SWFs). SWFs have AUM worth trillions of dollars globally.

- Pressure on risk assets from SWF selling.

- Significant savings for oil-importing nations. The question is what will they use the surplus for?

- Corporate bankruptcies should build gradually as “lower for longer” prices continue to hurt producers.

- Whole nations can go bust. Venezuela is likely to do so with Nigeria, Russia, Brazil, Angola all facing troubles, albeit on different scales.

- The scramble for Dollars is driving the price of the Greenback higher leading to a “vicious circle” in liquidity

The net global effect currently looks decisively deflationary as the savings are mostly spent on paying down debt by favored nations and consumers while producers are cutting back on investments as they try to survive the slump. The cash-strain forced a lot of producers to actually increase production to stay afloat further exaggerating the decline. The effect of shrinking SWFs is unclear but it can definitely play a major part in the strong sell-off in risk assets this year.

Supply and Demand

EIA estimates that inventories, already at record highs, will continue to build throughout 2016 as the disconnect between supply and demand will likely diminish gradually. We have to add that demand is fragile in the current economic situation and the pick-up in growth that the agency forecasts for the second half in 2016 is questionable.

On the plus side, a looming inventory crisis (as storage capacities are filling rapidly) may help in sorting out the supply glut the hard way by pushing down short-term prices into an unsustainable territory and forcing less-efficient producers out of the business. We will soon take a look at the break-even point for various players to have a better understanding of the situation.

Super-contango and safe(r) ways of playing the bottom

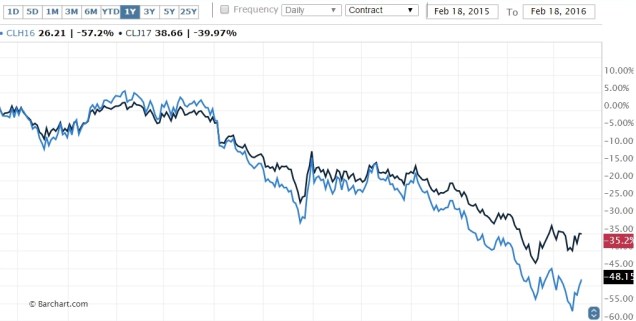

As the short-term fears are growing the best clue for a bottom should be the different behavior of futures contracts with expiries in the near future and further out. Contango is the phenomenon of future prices being higher than the current ones, like most of the times in the case of oil futures.

The interesting thing is the change in the difference between current and future prices. As the immediate stress grows (think about the inventory build) spread could widen dramatically and provide evidence of a coming change in the trend (or at least of reduced pressure on prices).

Also, the public’s focus on the front contract means that sentiment can become overly bearish as the near-term expiries crash but long-term prices stay relatively stable.

Let’s take a look at the current situation!

The above chart shows the YTD performance of the March 2016 WTI contract (black line) and the April 2017 contract. As you can see the difference not only got much higher (above $10 dollars a few days ago) but as this year’s contract made new lows in February the 2017 contract stayed above its January levels.

Now this doesn’t mean that the bottom is in at all. We have seen one-year super-contangos over $20 before but the extent of the recent moves and the excessive negative sentiment could point to a bottom not too far in the future. So monitoring the situation while searching for candidates, and maybe building a core position in the best names might be the way to go here.

Playing a possible rebound

Betting on the oil price itself is probably not the safest way of playing a rebound. As the current stress subsides but the oversupply remains intact, long-term contracts might drift lower as the contango eases. The better ways include buying strong businesses that are profitable even in the current environment and will likely gain market share as weaker players are forced out.

Also looking for companies in countries where the currency significantly devalued (e.g.: Russia, Brazil etc.) is not a bad idea, as long as the firms are not indebted in foreign currencies, have their production costs in local currency, and have a diversified customer base with preferably a high level of exports.

- Look for companies with strong assets and healthy balance sheets.

- Hedged producers have a great advantage in the current set-up.

- Integrated companies with ample liquidity will be able to buy distressed assets helping future growth.

Don’t forget that some of those who survive will emerge from the cyclical downturn stronger than they were before. If you stick to these filters you will have investments with good return/risk profiles, without having to worry about short-term prices.

The takeaway

So to wrap-up our current view on oil, fundamentals are still weak and the disparity between supply and demand is intact. Still, there are signs that the market is getting close to clearing the excesses (in price) and although the pain is likely to continue in the foreseeable future the time might be just right to look for investment targets. Stay tuned for our detailed look at some of our favorite companies in the segment!

Let us know what you think in the comments section and don’t hesitate to add your own insights, we surely missed a lot!

Great trading and investing for all! Stay safe out there!

StockMate